Dear Partners,

As we’ve often said in previous letters, we couldn’t be more excited about the current business environment. The next five years could yield some incredible opportunities for us as investors.

During periods of inevitable market declines, such as the one we just experienced, it’s important to remember that we own businesses—not just stocks. Stock prices go up and down, and the market often behaves irrationally in the short-term based on fleeting sentiments.

On the other hand, healthy and growing businesses do not fluctuate nearly as much as their stock prices.

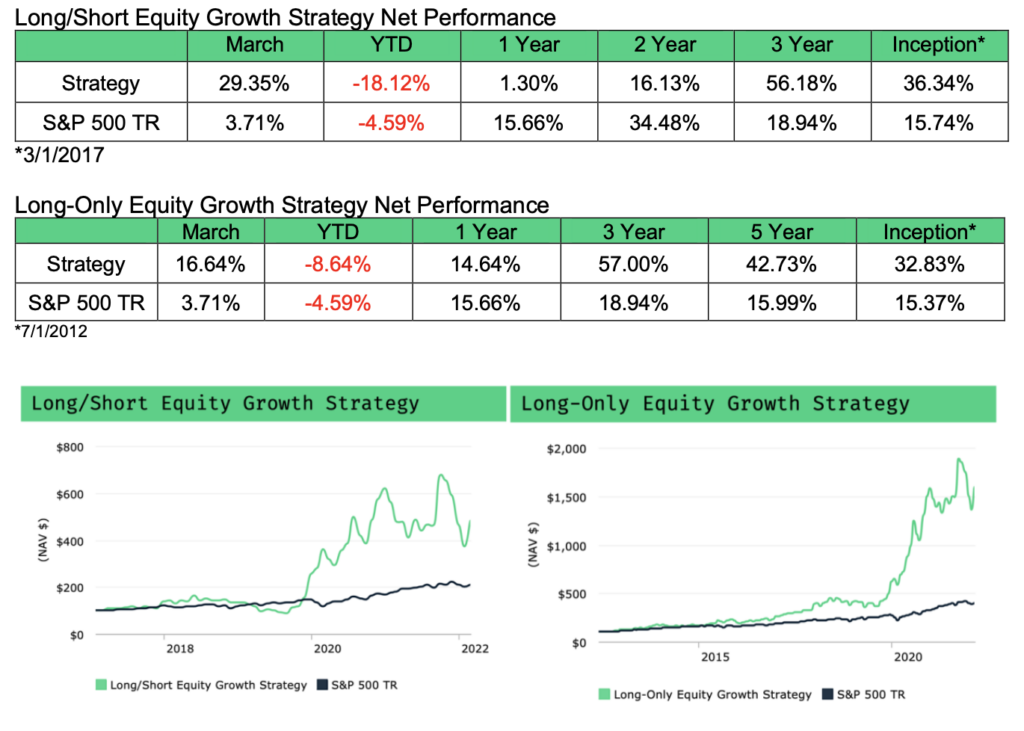

Please see here for composite presentations for additional information and disclosures.

Our philosophy is predicated on this simple idea: The best strategy to mitigate against investment risk over the long-term is to strive to own the #1 companies in their respective fields. We think this strategy offers us a significant margin of safety, regardless of what prices are telling us on any given day.

This is key: Whether we own one business, five businesses, or even 20 businesses, we take risk off the table by owning quality, real companies that will survive and thrive in any environment.

Our process is built around an intense, multi-year research effort into a few select industries undergoing significant changes. And our goal, simply put, is to develop an immense level of conviction on which businesses are best poised to dominate the competition, emerge triumphant, and outperform expectations.

While the last 12 months have been challenging, the truth is, we love this current setup. Our businesses are performing well. We are delighted with their progress, and we see many positive years ahead for us.

The “Innovation Bubble”

This recent drawdown has been particularly vicious to certain segments of the market. Take a broad basket “innovation” ETF like ARKK. As of this writing in April 2022, ARKK is down some 60% from its highs. Other high-growth public companies have completely roundtripped back down to 2018 levels. These types of drawdowns don’t happen very often, but they do indicate that there was perhaps too much speculation that needed to be purged from the market.

Going forward, dominant companies should thrive in this environment. By flushing out the weak hands, we think the market has forced investors to concentrate capital into the top companies with real value propositions. From our perspective, many companies that got caught in the 2021-22 “Innovation Bubble,” as we might call it, may never reclaim the values they once had.

Others, however, will stand the chance to compound at incredible returns going forward. Just as Pets.com never recovered from the Nasdaq bubble, other companies, such as Amazon, went on to become trillion-dollar conglomerates. We think that’s the environment we’re in today.

The fact is, markets can be quite predictable if you take a long enough view of history. Every six or 10 years, a major decline shocks the market. Sometimes these declines affect the broader indices, and sometimes—such as the Nasdaq bubble and the “Innovation Bubble”—declines are concentrated within certain sectors.

The cause of these bubbles forming, and popping, is almost beside the point. We can debate the causal effects of quantitative easing, interest rates, inflation—it ultimately doesn’t matter. The point is this: Some companies may never regain their peak valuations. Other companies, on the other hand, will likely go on to 10x, 100x, and even 1,000x based on their fundamental business performance and their ability to generate cash flows.

It’s an exciting time, to say the least. We’re even more bullish on our core holdings than we were a year ago. Major declines are relatively rare, and almost always followed by five to 10 years of “good times,” in our experience.

For stock pickers, this creates a wonderful environment to find value.

Some portfolio and research updates

Over the last several months, we have become increasingly bullish on Tesla, our largest holding. As an expression of our increased confidence, through Q1 we increased our Tesla position.

At a high level, we believe Tesla is on a path to dominate the S&P 500. Much like Amazon emerged from the Nasdaq Bubble and the Financial Crisis, we think Tesla has at least another 10 years of growth ahead, and it is just now hitting its inflection point of accelerated, rapid growth.

At the same time, consensus estimates of Tesla’s growth are, in our view, extremely low. This dynamic, in our opinion, will likely result in consistent upwards revisions to expectations, creating one of the more dramatic arbitrage investment opportunities we have ever come across.

From a data, scale, and advanced manufacturing perspective, the company is entering escape velocity. To be clear, Tesla’s stock price and market value is no longer a reflection of anticipated success. It reflects its current success and proven ability to generate substantial earnings and record-setting cash-flows at scale. In sum: It’s early days. We’ll soon be publishing a comprehensive research report on Tesla. Stay tuned.

Spotify, another core holding, has dramatically underperformed in the market, falling ~37% in the first quarter and fully-roundtripping to its direct listing price in 2018, which has dragged down our overall performance.

Despite the underperformance of the stock, we are fundamentally bullish on the company and its prospects going forward. Like our experience with Tesla in 2019, Spotify is facing investor scrutiny about its path to profitability, increased competition, and even some cultural flare-ups that captivated the media and investors (i.e. Joe Rogan). Also like Tesla in 2019, our internal price targets keep going up while the stock price keeps faltering.

Here is the reality: We believe Spotify is one of the most relevant platforms in existence today, and in our view, it faces a very good chance of eclipsing the value of Netflix (currently ~$152b) over the next several years. At a current market value of less than $27 billion, we have ample runway ahead.

Spotify is building the global audio infrastructure of the Internet, which we believe will enable a large influx of high-margin revenue through advertising and direct monetization. Just as video content is a trillion-dollar opportunity, we view audio through a similar lens.

At a recent investment conference, Paul Vogel, Spotify’s CFO, commented about the long-term profitability of what Spotify is building. “The opportunity in front of us is still massive,” he said. “Like you said, we’re at 400 million users. We think we can get to 1 billion… there’s ways to grow gross margin, [and] we believe we have a path to get there. And so there’s two ways to do it: one is to properly tell our story, which we will do; and then two is just deliver the results.”

We agree.

Closing thoughts – the future

As we often say, we think this decade will be a stock picker’s market—especially in today’s environment. The companies that can execute going forward will be rewarded. Others will not. Bursting bubbles create many tremendous bargains, but it’s important to remain selective. Though valuations have come down, certain companies that appear “cheap” can still be deceiving.

As always, we are thankful to have you as partners alongside us in our firm. We remain exceedingly optimistic about the next several years, and the ability to generate significant absolute returns going forward. The returns along the way may be lumpy, but the rewards will justify the means.

Despite the gloom that you come across—in the news, in the markets—this is a fantastic time to be an investor. The next several years will provide some profoundly attractive opportunities.

We are excited and focused on the road ahead.

Sincerely,

Nightview Capital

Arne Alsin – Founder, CIO + Portfolio Manager

Zak Lash, CFA – COO

Daniel Crowley, CFA – Director of Portfolio Management

Eric Markowitz – Director of Research

Philip Bland – Director of Investor Relations

Emily Bullock – Head of Compliance

Cam Tierney – Research Analyst

**Disclosures

This has been prepared for information purposes only. This information is confidential and for the use of the intended recipients only. It may not be reproduced, redistributed, or copied in whole or in part for any purpose without the prior written consent of Nightview Capital. The opinions expressed herein are those of Nightview Capital and are subject to change without notice. The opinions referenced are as of the date of publication, may be modified due to changes in the market or economic conditions, and may not necessarily come to pass. Forward looking statements cannot be guaranteed. This is not an offer to sell, or a solicitation of an offer to purchase any fund managed by Nightview Capital. This is not a recommendation to buy, sell, or hold any particular security. There is no assurance that any securities discussed herein will remain in an account’s portfolio at the time you receive this report or that securities sold have not been repurchased. It should not be assumed that any of the securities transactions, holdings or sectors discussed were or will be profitable, or that the investment recommendations or decisions Nightview Capital makes in the future will be profitable or equal the performance of the securities discussed herein. There is no assurance that any securities, sectors or industries discussed herein will be included in or excluded from an account’s portfolio. Nightview Capital reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs. Recommendations made in the last 12 months are available upon request. Past performance Is not indicative of future results. Returns are presented net of investment advisory fees and include the reinvestment of all income. The S&P 500 Total Return is a market-value-weighted index that measures total return, including price and dividends, of 500 leading companies in leading industries in the U.S. economy. The volatility (beta) of the accounts may be greater or less than benchmarks. It is not possible to invest directly in this index. Nightview Capital, LLC (Nightview Capital) is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Nightview Capital including our investment strategies and objectives can be found in our ADV Part 2, which is available upon request. WRC-22-02